Link to the paper: Link

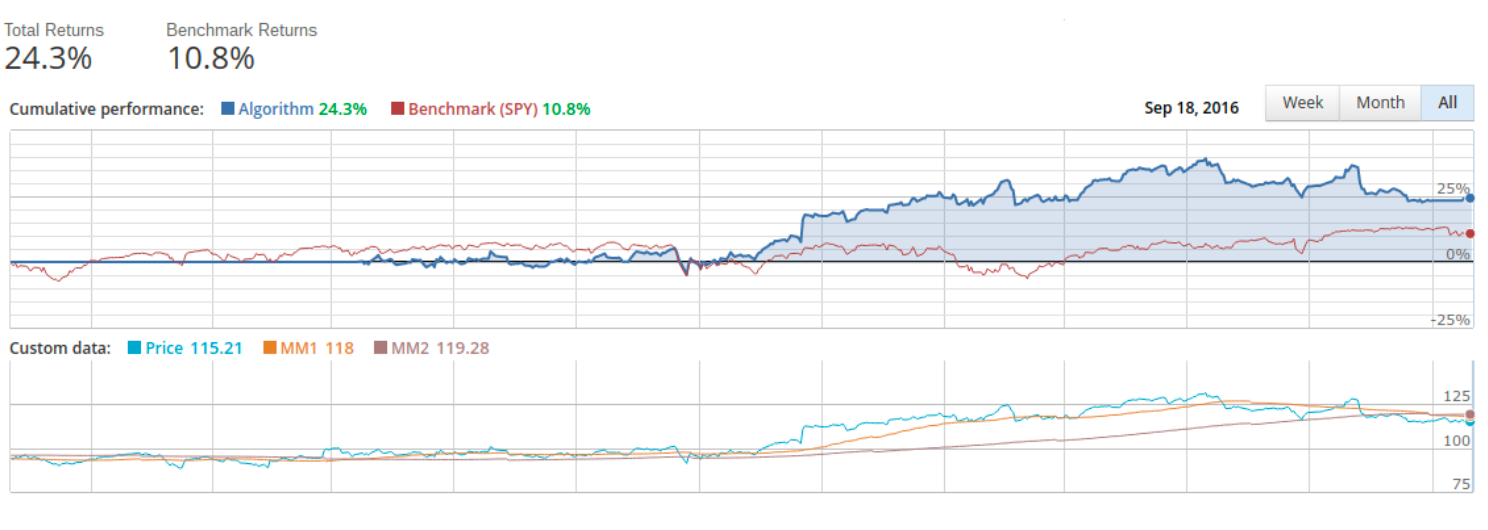

This is a small algo strategy I've designed with Python in 2015 back when Quantopian was still around. It was for a final paper at my University where I explained the history and model of electronic capital markets to then show what could be done with this new technology.

Image of price movement

Python and Quantopian's Zipline Library