Rust-powered collection of financial functions.

PyXIRR stands for "Python XIRR" (for historical reasons), but contains many other financial functions such as IRR, FV, NPV, etc.

Features:

- correct

- blazingly fast

- works with different input data types (iterators, numpy arrays, pandas DataFrames)

- no external dependencies

pip install pyxirr

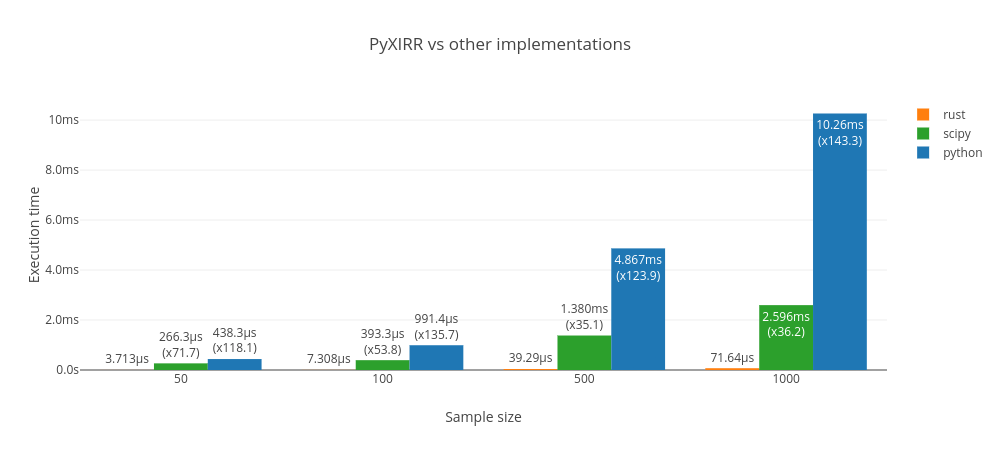

Rust implementation has been tested against existing xirr package (uses scipy.optimize under the hood) and the implementation from the Stack Overflow (pure python).

PyXIRR is ~10-20x faster in XIRR calculation than the other implementations.

Powered by github-action-benchmark and plotly.js.

Live benchmarks are hosted on Github Pages.

from datetime import date

from pyxirr import xirr

dates = [date(2020, 1, 1), date(2021, 1, 1), date(2022, 1, 1)]

amounts = [-1000, 750, 500]

# feed columnar data

xirr(dates, amounts)

# feed iterators

xirr(iter(dates), (x / 2 for x in amounts))

# feed an iterable of tuples

xirr(zip(dates, amounts))

# feed a dictionary

xirr(dict(zip(dates, amounts)))

# dates as strings

xirr(['2020-01-01', '2021-01-01'], [-1000, 1200])Numpy and Pandas support

import numpy as np

import pandas as pd

# feed numpy array

xirr(np.array([dates, amounts]))

xirr(np.array(dates), np.array(amounts))

# feed DataFrame (columns names doesn't matter; ordering matters)

xirr(pd.DataFrame({"a": dates, "b": amounts}))

# feed Series with DatetimeIndex

xirr(pd.Series(amounts, index=pd.to_datetime(dates)))

# bonus: apply xirr to a DataFrame with DatetimeIndex:

df = pd.DataFrame(

index=pd.date_range("2021", "2022", freq="MS", closed="left"),

data={

"one": [-100] + [20] * 11,

"two": [-80] + [19] * 11,

},

)

df.apply(xirr) # Series(index=["one", "two"], data=[5.09623547168478, 8.780801977141174])Other financial functions:

import pyxirr

# Future Value

pyxirr.fv(0.05 / 12, 10 * 12, -100, -100)

# Net Present Value

pyxirr.npv(0, [-40_000, 5_000, 8_000, 12_000, 30_000])

# IRR

pyxirr.irr([-100, 39, 59, 55, 20])

# ... and more! Check out the docs.See the docs

- Implement all functions from numpy-financial

- Improve docs, add more tests

- Type hints

- Vectorized versions of numpy-financial functions.

- Compile library for rust/javascript/python

Running tests with pyo3 is a bit tricky. In short, you need to compile your tests without extension-module feature to avoid linking errors.

See the following issues for the details: #341, #771.

If you are using pyenv, make sure you have the shared library installed (check for ${PYENV_ROOT}/versions/<version>/lib/libpython3.so file).

$ PYTHON_CONFIGURE_OPTS="--enable-shared" pyenv install <version>Install dev-requirements

$ pip install -r dev-requirements.txt$ maturin develop$ LD_LIBRARY_PATH=${PYENV_ROOT}/versions/3.8.6/lib cargo test --no-default-features --features tests$ pip install -r bench-requirements.txt

$ LD_LIBRARY_PATH=${PYENV_ROOT}/versions/3.8.6/lib cargo +nightly bench --no-default-features --features testsThis library uses maturin to build and distribute python wheels.

$ docker run --rm -v $(pwd):/io konstin2/maturin build --release --manylinux 2010 --strip

$ maturin upload target/wheels/pyxirr-${version}*